Financial Accounting for Beginners: A Simple Guide

Financial accounting is the systematic process of documenting, summarizing, and presenting a company’s financial activities. It involves gaining data, organizing it into financial statements, and then evaluating the results to gain insight into the company’s financial performance. This information is critical for client decision-making, including for investors, creditors, and management. In essence, financial accounting provides an accurate picture of a company’s financial status and activities.

Understanding Financial Accounting

Financial accounting is the process of recording, summarizing, and reporting on a business entity’s financial operations. It entails the creation of financial statements such as the income statement, balance sheet, and cash flow statement.

These statements offer stakeholders information about the organization’s financial health and performance, allowing for better decision-making and responsibility. Financial accounting uses generally recognized accounting principles (GAAP) or international financial reporting standards (IFRS)

What is Financial Accounting?

Financial accounting is the discipline of accounting that records, summarizes, and presents a company’s financial information to external stakeholders. It entails meticulously recording corporate transactions, preparing financial statements such as the income statement, balance sheet, and cash flow statement, and following to standardized accounting rules like GAAP or IFRS.

The fundamental purpose is to offer investors, creditors, regulators, and other users with financial information that is credible, relevant, and understandable. Read this blog to learn about Digital Marketing Tools for Success Career.

Why Is Financial Accounting Important?

Financial accounting aids in determining critical variables such as debts, obligations, assets, and property, providing a comprehensive picture of the company’s financial health.

- Financial Reporting

It provides an organized method for recording, summarizing, and reporting financial transactions in a business. These reports, such as the balance sheet, income statement, and cash flow statement, help stakeholders such as investors, creditors, regulators, and management understand the company’s financial health and performance.

- Decision Making

Accurate financial data is critical for making educated decisions. Managers rely on financial statements to assess the financial health, liquidity, and general performance of the business. To enhance your English, check out the How to Learn English Fluently blog. Investors use financial reports to assess the possible rewards and risks of investing in a specific firm. Creditors analyze financial documents to determine a company’s creditworthiness before giving loan.

- Investor Confidence

Transparent and honest financial reporting increases investor confidence. Investors are more willing to invest in companies that provide accurate financial data. Also, publicly traded corporations must disclose financial information to the public, which promotes trust and confidence among investors and stakeholders.

- Performance Evaluation

Financial accounting enables firms to analyze their performance over time by comparing financial data from various eras. This helps to detect trends, strengths, and weaknesses, allowing management to make strategic decisions to increase performance and efficiency.

Key Concepts and Terminology

Balance sheet accounts are assets, liabilities, and owners’ equity. Income statement accounts are revenue and expenses. Accounts are classified as permanent or temporary. Permanent accounts, also called real accounts, are balance sheet accounts that remain open from the accounting period to the accounting period.

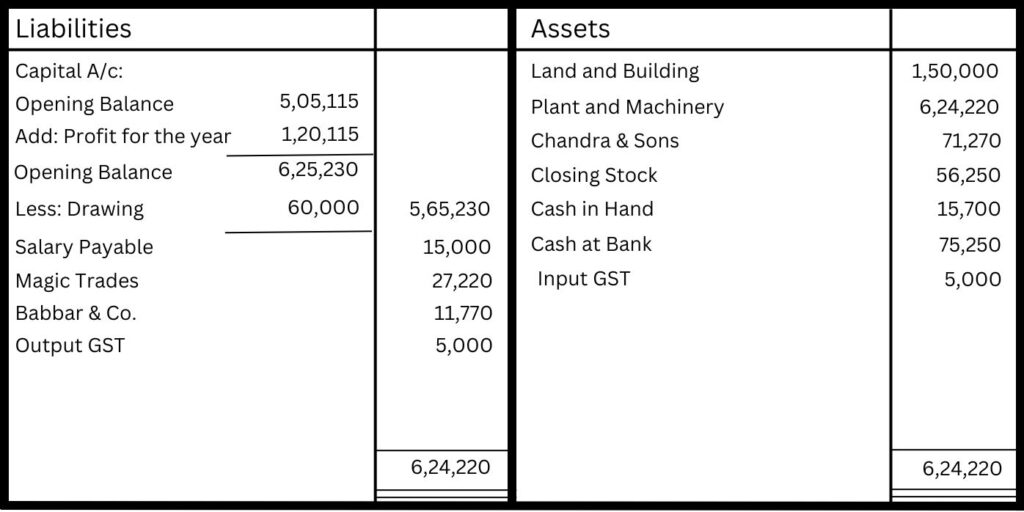

Liabilities in financial Accounting

Liabilities mean amount owed payable by the business. Liability towards the owners of the business is termed as internal liabilities. On the other hand, liability towards the outside, i.e. other than the owners is termed as external liability.

External liability arises because of credit transactions or loans taken. Examples of external liability are creditors, bank overdraft, long-term borrowings, and other liabilities. Liability is further classified into.

- Non- current Liability : Non- current liability is that liability which is payable after a period of more than a year from the end of the accounting period. Examples of Non- current Liability are long-term loans, debentures, etc.

- Current Liability : Current Liability is that liability which is payable within 12 months from the of the accounting period. Examples of current Liability are creditors, bills payable, short-term loans, etc.

Assets in financial accounting

Assets are the properties owned by an entity or enterprise. They are the economic resources of the business. In other words, anything which will enable the firm to get economic benefit in the future, is an asset. Examples of assets are land, building, machinery, furniture, stock, debtors, cash and bank balance, trademarks, copyrights, goodwill, etc.

- Non-Current Assets : Non-current are those assets which are held by an entity or enterprise not with the purpose to resell but are held either as investment or to facilitate business operations.

- Fixed Assets : Fixed Assets are those non- current assets of an enterprise which are held not to resell but with the purpose to increase capacity.

Account for Financial Accounting

It is record of transaction (cash and credit) under a particular head of account or a particular head (say asset, liability, etc.). It not only shows the amounts of transaction but also show their effect and direction.

Drawings

It is the amount withdrawn or goods taken by the proprietor or partner for personal use. Goods so taken by the proprietor are valued at purchase cost.

Profit

Profit means income earned by the business from its Operating Activities, i.e., the activities carried out by the enterprise to earn profit. For example, Profit earned from sale of goods and/or rendering of services.

Loss

Loss is excess of expenses of a period over its revenues. It decreases the owner’s equity. It is a broad team and includes loss incurred in its operating no benefit.

Gain

Gain in the increase in owner’s equity resulting from something other than the day to day earning from irregular or non-recurring nature. stating differently, it is a profit that arises from transactions which are not the Operating Activities of the business but are incidental to it such as gain on sale of land, machinery or investments.

Income

Income is the profit earned during an accounting period. In other words, the difference between revenue and expense is termed as income. It is broader term then the term ‘profit’ and includes profit from activities other than its Operating Activities.

Principles of Financial Accounting

The principles of financial accounting include documenting, summarizing, and reporting financial transactions in accordance with generally accepted accounting principles (GAAP). The accrual foundation, matching principle, consistency, materiality, and conservatism are key concepts that ensure accurate and reliable financial data for decision-making and external reporting.

Generally Accepted Accounting Principles (GAAP)

Generally Accepted Accounting Principles (GAAP) are a collection of standardized accounting principles, rules, and procedures that businesses utilize to prepare financial statements. GAAP is a framework for preparing and presenting financial statements that ensures uniformity, comparability, and honesty in financial reporting.

Financial Accounting Relevance

Financial data should be relevant to the decision-making needs of users. It should allow users to evaluate past performance, project future outcomes, or both.

Reliability

Financial information should be credible, verifiable, and accurately reflect the economic substance of transactions. This includes ensuring that financial reporting is accurate, full, and neutral.

Comparability

Financial statements should be comparable within the same entity across time and between companies. This facilitates the examination and understanding of financial performance and position.

Prudence (Conservatism)

When dealing with uncertainty, accountants should proceed with prudence, recognizing losses and liabilities as soon as they are likely and earnings and wealth only when they are certain.

Double-entry in financial accounting

double Entry System of accounting under which both, debit and credit, aspects of accounting are transaction has two aspects-Debit and Credit-and at the time of recorded on the credit side. For example, at the time of cash pucheses, goods are received and in return cash is paid. In the transaction, two aspects are involved, i.e., receiving goods and playing cash and under the Double Entry System, both these aspects are recorded.

Feature of the Double Entry System

- It maintains a complete recode of each transaction.

- It recognises two -fold aspect of every transaction, uiz., the aspect of receiving and the aspect of giving.

- In this system, one aspect is debited and the other aspect is credited following the rules of debits and credit.

Stages of Double Entry

A complete System of double entry book keeping has following three stages:

- Recording the transactions in the Journal.

- Classifying transaction in the journal by posting them to the appropriate ledger accounts and then preparing the Trial Balance.

- Closing the book and preparing the final accounts.

Accrual vs. Cash Basis Accounting Financial

Cash accounting only records revenue and expenses when money changes hands, whereas accrual accounting recognizes income when earned and expenses when billed (but not paid).

Accrual Basis Accounting

- It gives a more accurate view of a company’s financial status because it includes all financial activity, including credit transactions.

- Accrual accounting is often necessary for organizations that exceed specific sales criteria or have inventory because it provides a more complete picture of financial performance over time.

Cash Basis Accounting

- It is simpler and easier to implement than accrual basis accounting, making it ideal for small enterprises and individuals with minor financial activities.

- Cash basis accounting does not accurately reflect a company’s financial performance since it does not account for transactions that have been promised but not yet completed, or expenses that have been incurred but not yet paid.

Financial Statements Overview

Financial statements are written records that summarize an organization’s business operations and financial performance. In most circumstances, they are audited to verify their correctness for taxation, finance, or investment purposes.

Balance Sheet

The balance sheet is a fundamental financial statement that organizations use to present a picture of their financial condition at a specific point in time, usually at the conclusion of a reporting period such as a quarter or fiscal year. It depicts the company’s assets, liabilities, and shareholders’ equity using the fundamental accounting equation:

Income Statement

- The income statement, also known as the profit and loss statement, displays a company’s sales, expenses, and net income over a given time period, such as a quarter or a year.

- Net income is the difference between sales and expenses that shows the company’s profit or loss for a certain time.

Cash Flow Statement

- The cash flow statement summarizes the cash inflows and outflows from operating, investing, and financing operations during a certain time period.

- Operating activities involve cash receipts and payments for day-to-day business operations, such as sales revenue, supplier payments, and salaries.

- Investing operations include cash flows from the purchase and sale of long-term assets such as real estate, plant, and equipment.

- Financing activities include cash flows from borrowing and repaying debt, issuing and repurchasing stock, and paying dividends.

Statement of Stockholders' Equity

The Statement of Stockholders’ Equity summarizes the changes in a company’s equity over time. It often includes information about initial investments, retained earnings, dividends, and other factors that affect shareholders’ equity. This statement explains changes in the company’s ownership structure and the distribution of profits to shareholders.

Analyzing Financial Statements

Financial statement analysis is the process of studying a company’s financial statements to help make decisions. External stakeholders use it to assess an organization’s general health, financial performance, and business value. Internal constituents utilize it to monitor and manage their finances.

Ratio Analysis

Ratio analysis is a key tool for assessing a company’s financial performance and health. By measuring and evaluating numerous financial measures, stakeholders can gain insight into liquidity, profitability, solvency, and efficiency. These ratios give a comparative examination of key financial parameters, allowing investors, creditors, and management to identify a company’s strengths and weaknesses.

Ratio analysis is useful in decision-making processes such as investment evaluation, credit risk assessment, and strategy planning, allowing stakeholders to make educated judgments regarding a company’s future prospects.

Common Size Analysis

Common size analysis is a technique for evaluating financial statements that expresses line items as a percentage of a base figure, which is usually total revenue (for income statements) or total assets (for balance sheets). By standardizing financial data in this manner, analysts can examine the relative quantities of multiple elements inside the identical statement of finances or over periods of time.

Common Analysis

Common size analysis is a technique for evaluating financial statements that expresses line items as a percentage of a base figure, which is usually total revenue (for income statements) or total assets (for balance sheets). This provides for a more meaningful comparison of financial performance and aids in the identification of trends, outliers, and areas that need additional research or improvement.

Recording Transactions

Recording transactions is a simple accounting process that involves only a few stages. The first step is to identify the transaction and the accounts that it will affect. The second step is to register the actions taken in the proper accounts. When entering numbers into the debit and credit areas, careful consideration is required.

Debits and Credits

Debit refers to the left side of an account and credit refers to the right side of an account. In the abbreviated from Dr. stands for credit. An item recorded on the debit side of an account is said to be debited to the account. An item recorded on the credit side of an account is said to be credited to the account.

Both debit and credit may represent either increase or decrease depending upon the nature of an account. The rules of debit and credit depend on the nature of account.